Starting off with addressing the main points quickly - Trump is to take office in the US in around 2 weeks from now, whilst there is still little concrete evidence of what exactly he will do, regarding fiscal policy the consensus is for a large impulse. Given how little detail is still known, its hard to determine the impact but banks have given a stab at it, and the table below shows the consensus shift that has occurred to stronger growth/inflation/activity. SG were admittedly rather bearish before trump, with '19 GDP effectively forecast at flat, though the introduction of Trump's policies is seen to raise GDP by 1.1pp y.y through 2018/19. Ranges of estimates from various banks sit somewhere around this, with some as low as +0.4pp.

|

| Pre/Post Trump forecasts, from SocGEn |

|

| Number of hikes priced into Fed Funds curve for 2017 |

The first main concern is how realistic this is to occur, markets have flipped and people are now paying global rates as the perceived benefit from trump meaningfully changes things...

Firstly, it still feels rather presumptuous that the benefits from the changes in policy will outweigh the costs. It's true that the world has been relying on monetary policy for too long as this panacea of growth and its a good thing that governments will be shifting more towards fiscal policy, hopefully a similar thing can be done in Europe. But going back to Trump, and his outright protectionist measures, clear disdain for China and Mexico is surely going to be negative for Emerging markets, the very areas that have done lots of the heavy lifting post 2008.

Thus far EM has remained robust. FX took an immediate hit of a few %, but credit (CDX EM, inverted) has remained very strong, trading just shy of tightest levels of 2016. Room for further weakness when/if the full extent of Trump policies are known.

|

| EMFX index and CDX EM |

Secondly, global rates still remain rather anchored to or below 0. Both the ECB and BoJ have moderately shifted their viewpoint to negative rates throughout 2016 as the backlash on banks and the upward pressure from US rates leading to "tapering" from the ECB (which was hardly tapering but ok) and yield curve control from the BoJ. But these have been small shifts and will keep a lid on JGBs and Bunds going forward, so one does continue to question how far US yields can diverge before the pressure becomes too great. Bearing this in mind, historical spreads between US and Japanese 10 years have reached close to 5% (4.93 in 2000), and currently only stand at 2.4% where as Bund/UST spread stands at its widest in history. The first issue with these continuing to widen is the feedback loop to the USD...

The FOMC in their Dec meeting minutes started to express concern for a strong USD, however one can infer the pressure is not great enough for concern just yet. But it will build. Secondly, global flows will inevitably favour owning US rates, either FX hedged or not. If the consensus builds that the USD will certainly rally (which is the consensus) there will be less pressure to hedge fx and will keep global rates anchored still as international investors pick up USTs.

|

| Yield spread vs EURUSD (inverted to show USD strength) |

A 10y UST fx hedged to a Japanese investor offers yields 55bps higher than a JGB

|

With these considered, I think longer end rates remained somewhat anchored together, but still believe there is room for this trump narrative to play out much more, easily to 3% on 10s before the feedback loops and negative impacts on RoW are felt.

With this also, EURUSD does seem like it will finally crack parity this year, something which I hate to jump on as those that have followed my previous EURUSD trades, I have faded below 1.07 for the past 2 years, and hate to be with consensus here.. but feel that the momentum behind the trump narrative can run further into his reign whilst risks politically in europe are only getting louder in 2017, with Le Pen a sizable concern at the back of my mind right now. As such, I do like owning 3/6month parity options.

As writing with spot at 1.0520, a 6 month 1.00 Digi put costs 20%, offering up a 4:1 risk/reward, which seems worth owning. Other ideas could be put ladders, as skew has cheapened in the past month.

|

| EURUSD 6m 25delta RR |

In the meantime, the pressure that US rates have had on other markets certainly has created good opportunities. Looking to markets such as Swedish front end rates.

Global curve steepening has meant forward rates trade at quite a premium, with hefty rolldown. Sweden very notably with SEK 1y1y trading at the higher end of its yearly range at -0.2% and vs a 1y swap at -0.5%, offering 30bp of roll down all else equal.

|

| SEK 1y1y |

The Riksbank remain extremely dovish, and with a strong dislike for a strong SEK, in recent weeks however TWI SEK has rallied >3% as EURSEK rejected 10. Whilst only back to levels earlier on in the year, the direction of travel is against their plan and expect to see murmurs to suggest against a continued rally. Unfortunately the riksbank are quite reactionary to the ECB with regard to policy, and frankly will continue to do this almost as if they were pegged to the EUR.

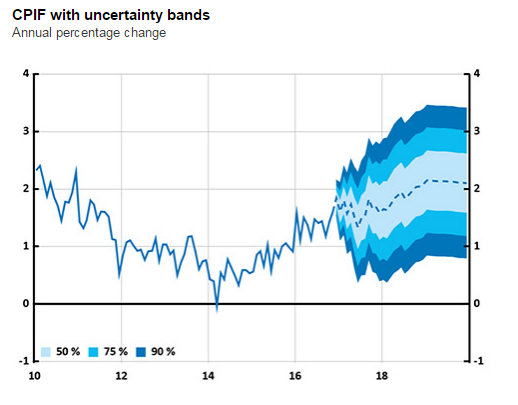

|

| Sweden CPIF forecasts |

Domestic data however is strong in Sweden, with upward pressures to inflation and steady growth, declining u/e, however the pull factors from the ECB will outweigh any potential domestic out-peformance for the foreseeable future, and the repo rate is not expected to rise until 2018 at the very earliest based on the Riksbank's on estimates. Something they will not want to bring forward as impacts on the FX will be detrimental.

One trade to pair this with, which creates a well balanced European rates long/short.

Paying EUR 10s30s at 58bps here, offers 15bps of carry/roll in a year, for a curve which typically has an annual range of 50bps.. thus a strong curve steepener with great carry/vol.

|

| SEK 1y1y vs EUR 10s30s |

Based on this historical beta, could also weight each leg roughly 1:2. Receiving 5k dv01 of SEK for every 10k of paying EUR.

Elsewhere, and another cheap area to receive rates is AUD/NZD and whilst is a similar set-up to SEK, has different associated risks, namely more commodity and EM related.

So when considering how the RBA reacts going forward will to a large degree depend on how China and global EM responds to trump, if there is more pain to come both through financial markets and economic data, then the balance of risk is skewed to cuts rather than hikes. Currently 18bps of hikes are priced in the AUD curve through to Dec '17, and 54bps by Dec '18. Whilst remaining issues such as housing, and consistent economic performance (more notably in NZ) suggest cuts are limited, rhetoric from the CBers as well as the balance of global risks suggests value here. Owning either IRz7 or ZBZ7 (illiquid af tho) acts well as a china tail risk hedge.

|

| IR1 vs IR Dec 17 |

Outright though we still run the risk of a further sell off in US rates, as such playing this against EDs probably remains the best view, though starts to cost in roll.. Z7 ED/IR spread trades at 50bps, which could easily tighten towards 0 throughout the year if 2.5 hikes starts to materialize.

Moving onto talking about China, its hard to know where we stand, though I remain mostly skeptical about any sustained rebound there and do believe it will continue to struggle. Interestingly in recent days CFETS has re-balanced their basket (away from USD), arguably giving them more scope to deval against RoW, as we should more and more ignore what USDCNY does. Forward points and overnight rates have once again been massively squeezed in the start of this year, like last hurting the consensus long USDCNH positions.

12m forward points remain extremely elevated at ~3500 points, (some 6% above spot), and would favour waiting for this to settle before shorting CNH as outflows are likely to remain strong.. I do question however if Trumps stance on China and the current 6% annual yield for buying CNH might actually make it a decent currency to own in 2017..

Me, loving being the contrarian can easily convince myself to fade a lot of 2016 moves, namely the cheapness now occuring in TRY, MXN and even GBP.. each of which can be argued to provide decent value / carry but as of now I would prefer to not touch them, my most preferred outcome for these would be a quiet start to 2017, with trump being mild, global growth not surprising either way, and owning some upside via cheapening vols.

|

| TRY REER vs Carry/vol |

With regard to Turkey, the geopolitical risks, US curve steepening and stronger USD have weighed considerably. Carry/vol is leading REER lower, and whilst seems cheap, needs carry/vol to improve before stepping in (or having giant balls with which to fade it).. Lots of complicated factors in turkey, many of which i am clueless too. But another considerable wash out would certainly whet my appetite to getting long.

One consensus trade in FX is being short CAD, and for a multitude of reasons, weak economic data, a dovish BoC against rates that are pricing in tightening. On the other hand, oil prices remain strong supporting ToT and data on the margin. Charted below, we can see that the pull factor from widening rate differentials and downside with Oil leaves USDCAD slap bang in the middle. Personally my viewpoint on Oil is that it will mostly struggle to rally significantly as supply imbalances are slowly leaving the market and even the OPEC "cut" was not a huge game changer, especially when considering US supply that can come online towards 60, personally would prefer to lean on a 40/60 range for 2017, with OPEC supporting dips and the US (and even the USD) keeping a lid on it.

With spot leaning at the 100dma and bottom channel that has defined price action for the past 6 months, I would prefer to own upside, as a downward break could lead to a quick flush towards 1.300. A 1.37/1.40 Call spread costs 0.45% and with vols fairly cheap (~9), acts well to lean on a catch up to rates and any further commentary to bring CAD rates back in line with reality.

In summary then, my ideas are fairly low conviction here (aside from SEK vs EUR which is med/high) but as we go through the early stage of a trump presidency, we can hope that the direction and size of any policy will become clearer and then can reassess, until then trying to stay relatively balanced with regard to outright global rates.

In summary then, my ideas are fairly low conviction here (aside from SEK vs EUR which is med/high) but as we go through the early stage of a trump presidency, we can hope that the direction and size of any policy will become clearer and then can reassess, until then trying to stay relatively balanced with regard to outright global rates.

Summary:

-Long 6m EURUSD digi put @ 20% (spot ref 1.0520)

-Rec Sek 1y1y at -0.2%

-Pay EUR 5s30s at 59bps

-Short EDz7 vs Irz7 at 50bps

- Long USDCAD call spread 1.37/1.40 (spot ref 1.3275)

.

Great post as always!

ReplyDeleteI have one question. How do you calculate 2017 hikes priced in?(FFG7-FFG8) is multiplied by what?

Hi, so assuming each hike takes the Fed funds up by 25bps, i take FFG6-G8 spread, so about 0.6 points and then divide by 0.25 to get a number of hikes priced in

DeleteThanks!

DeleteWe have a wide range of Live and Demo trading accounts for you to choose from. Our range of Live Live trading include Cent, Basic, Standard, VIP and Exclusive accounts.

ReplyDeleteLE-MERIDIAN FUNDING SERVICES. We are directly into pure loan and project(s) financing in terms of investment. We provide financing solutions to private/companies seeking access to funds in the capital markets i.e. oil and gas, real estate, renewable energy, Pharmaceuticals, Health Care, transportation, construction, hotels and etc. We can finance up to the amount of $900,000,000.000 (Nine Hundred Million Dollars) in any region of the world as long as our 1.9% ROI can be guaranteed on the projects.

ReplyDeleteLe-Meridian Funding Service -Email lfdsloans@lemeridianfds.com.

lfdsloans@outlook.com

(WhatsApp...+1-989-3943-740 Or Call +1-913-9518-145)

We have forex trading solution

ReplyDeletefor you. You will be able to reap several benefits including competitive spreads & our advanced dashboard. Use our solution.

As one of the largest global trading markets, the Forex Market allows trades happen round-the-clock through interbank currency market. online forex trading platform

ReplyDeleteHow Lemeridian funding service grant me a loan!!!

ReplyDeleteHello everyone, I'm Lea Paige Matteo from Zurich Switzerland and want to use this medium to express gratitude to lemeridian funding service for fulfilling his promise by granting me a loan, I was stuck in a financial situation and needed to refinance and pay my bills as well as start up a Business. I tried seeking for loans from various loan firms both private and corporate organisations but never succeeded and most banks declined my credit request. But as God would have it, I was introduced by a friend named Lisa Rice to Le_meridian funding service and undergone the due process of obtaining a loan from the company, to my greatest surprise within 48hrs just like my friend Lisa, I was also granted a loan of $216,000.00 So my advise to everyone who desires a loan, "if you must contact any firm with reference to securing a loan online with low interest rate of 1.9% and better repayment plans/schedule, please contact Le_meridian funding service. Besides, he doesn't know that am doing this but due to the joy in me, I'm so happy and wish to let people know more about this great company whom truly give out loans, it is my prayer that GOD should bless them more as they put smiles on peoples faces. You can contact them via email on {lfdsloans@lemeridianfds.com Or lfdsloans@outlook.com} or Text through Whatsapp +1-989 394 3740.