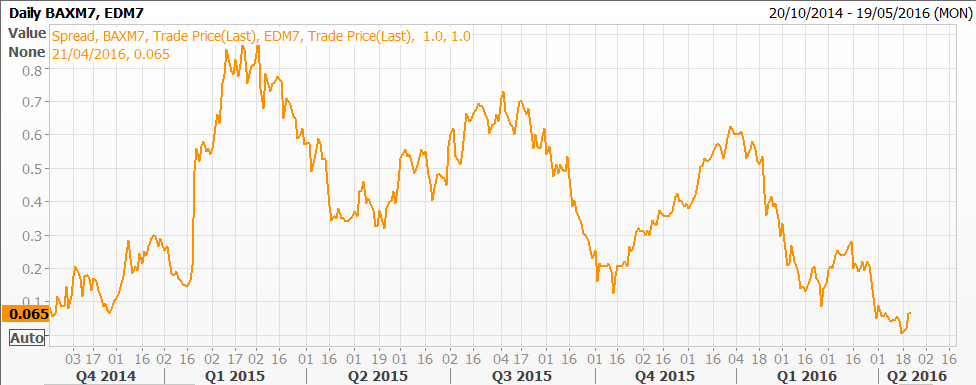

What is key for the Fed is not data, as much as they say so, its the SPX, its the VIX, its HY... Where each of these has seen a significant improvement. The S&P is back to 2100, the VIX is clearly sub 20, and chilling down in the low teens and HY spreads have improved dramatically, with CDX HY trading close to 400!

|

| CDX HY and VIX back to lows |

These combined, put the financial conditions in a better situation than last October, this generally feels like a repost of this article I wrote back in Oct.(http://macrocreditfx.blogspot.co.uk/2015/10/27th-october-fed-and-rbnz.html)

And once again, it definitely means that on the margin we should expect the Fed to surprise with a hawkish tilt going forward. Thus I look to position for a sell-off into next weeks FOMC.

Another factor that is seemingly now "bullish" is higher oil.. whilst a year ago, and according to the textbooks lower was better - but a goldilocks range for oil (and notably low volatility) is the most ideal situation here, especially for the HY/Shale types. This also takes pressure from declining inflation readings which once again on the margin should prove beneficial for US rate hikes this year.

For me now, the only main risk against a June Hike (excluding some unforeseen madness) would be Brexit... which could take place a week after the June meeting. Whilst I, and the market, sees a low (less than 25%) chance of a leave vote winning, it's a tail risk that the would hate to tighten into as it potentially causes political and economic issues in the worlds second largest economy. So this is what niggles at the back of mind as someone paying rates here.

Trade 1: 5s30s flattener at 135bps, targeting 120, risking a move above 140.

Here we can see the set-up, leaning on this downward trend, we can establish a flattener. Most of the leg work likely to be achieved from the 5s, which have seemingly rejected another move lower to 1% and have quickly headed towards the middle of the large 1-2% range. On the 30s, global anchorage of longer end rates remain to support duration and with the USD weakening a tad recently, there could be an increase in demand for longer end paper that pays some 2.7% in $s. When comparing against japan or europe, there is a significant yield pick up even after swapping out the ccy, and so real money flows from these would likely keep a lid on longer end rates. Alternatively, sell payers in 30s whilst selling recievers in 5s with a delta that is equivalent to a 5s30s flattener but gives us more optionality on the outcome, albeit with limited returns.

The main risk to this trade, aside from an overly dovish Yellen is a continued pickup in inflation expectations which put a greater pressure on term premium and the longer end of the curve. However inflation expectations have moved a lot which Oils leg higher so it may struggle to keep heading higher.

Trade 2: Buy $ 3m2y straddle against 3m10y

|

| Grey - 2s vol, Orange 10s, Blue 5s |

Trade 3: Buy Peripheral Debt vs Corporate HY

European HY markets have performed very well, with 5y Crossover trading at a mere 300bps, this compares to a comparatively wide levels for BTPs at 120bps.

The rationale for this trade is a normalization of BTPs as a risk proxy, but hedging out any potential market weakness by paying Xover. some causes for this divergence include a continued under performance of European Financials, specifically Italian and the inclusion of IG rate corporate credit into the ECBs buying program which has supported (indirectly) HY debt markets. This is a relatively low conviction, but lower risk trade.

Trade 4: Buy Canada STIR vs US at 6.5bps

|

| M7 STIR spread |

In FX, I have very little conviction anywhere. The EURUSD keeps flipping up and down in its range, whilst I am Bearish US rates, I am less bullish on the USD, and wouldnt be overly surprised to see us take out 1.15. In JPY, thats had a wild ride, where the market has called out the BoJ to a large degree of success so far, but one has to question with the improving risk backdrop / commodity price increase / BoJ that USDJPY downside is limited here.

AUDUSD remains bid with commodities (notably Chinese domestic metals are rocketting!) however as we approach 0.8 I start to see limited upside and the risk:reward is skewed to downside. EMFX and other EM assets have been very well supported by general risk sentiment and the recent Argy offering highlights the demand that is out there.

GBP is purely a brexit sentiment trade for the next two months as we hear more and more on polls, whilst staging a relief rally now (partly USD weakness), cable looks keen to burst higher through 1.44/1.45 however I'd expect to see hedgers and sellers re emerge and the upside on GBP is limited until we get *much* more clarity on what could happen.

Cross-asset vols broadly seem cheap to me, given the potential shocks and risks we see in the next 3 months, but very selectively will I buy vol. In US equity, it seems very cheap but the fed will try not to spook the markets here and whilst earnings are relatively lame, the market is shrugging it off.

I'm also visiting this site regularly, this web site is really nice and the users are genuinely sharing good thoughts.

ReplyDeleteCash

Hey friends, here is describe an rates thoughts. Nice author, Thank you. Need better advice ,just Go with instantForexSupport.com forum

ReplyDelete