But I just want to write a shorter piece for whilst at exams. Generally speaking, and maybe its because i'm arguably more focused on exams, I'm struggling more bigger thematic/directional ideas in the FX and Rates markets. However this maybe the dynamic we are in until the elusive rate hike.. which is now priced for Dec/Jan, and as such the markets are just in a "wait-and-see" mode. Either way, I'm not completely out of thoughts, just not as many as normal. The first thing to look at is obviously the EUR and bunds etc. Because they are still very much in the forefront of everyone's thinking.

|

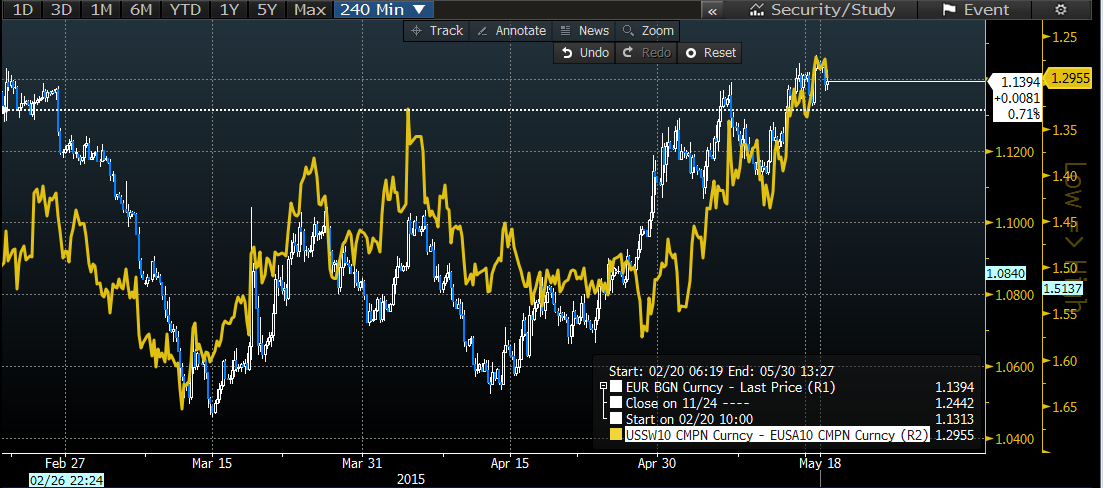

| EUR/USD vs US-EUR 10 year swap |

If you remember back a while, I positioned for a tighter spread, but now I think we've come in enough for that view to have diminished in the short run. I still think EUR long end rates should be higher, but I'm of course wary of the large QE flows etc.

Normally, the EURUSD rate is not too sensitive to the longer end spreads, but it seems clear from this overlay that it has been. Much the same reason i'm sure as to why the EUR is well correlated to the DAX for example. A lot of flows, both real money and CTA flow has been "hedged". Well this isn't new to anyone, we've all been talking about it for months, but it just still seems to be around, not sure for how long though, would expect this to diminish as markets settle down... (I'm not one for correlation trading lol, but would expect lower correlations going forward, and it intuitively makes sense)

|

| EURUSD vs DAX inverted |

Looking at ATM implieds in DAX and SPX, we can see the premium in VDAX is crazy high.

The skew is equally interesting, if you follow me on twitter, you would have seen my long SPX risk reversal trade, which is doing nicely, but I think that DAX is probably even more interesting. selling downside in the DAX is obviously risky, but probably worth it. I mean those of you that know me, know I'm a bit of a theta whore, but this does seem like good value especially going into the summer doldrums.

Furthermore, we see that Bund futures, have set-up, at least from a tech perspective, a bit of a base.

Potentially we could see a pop in RX which would likely be construed as EUR bearish assuming USTs are like meh.

Combining these, I can't help but end up with a shorter term EURUSD bearish bias. And this is strange coming from me, as I've been calling for it to pick up every since we dropped around 1.08 (just see older blog posts).. but we trade now, just shy of 1.14 and we may getting a bit ahead of ourselves, and if the lazy correlations remain then a move back towards 1.10 is on the cards for now.

In other FX markets, We've had time for the GBP to settle down, if you read back to my election piece here you'll see that I bought a zero-cost GBPUSD risk reversal, we currently sit ~800 points higher then when I recommended that and I've now covered.

|

| GBP vs STIR rates |

So that trade has done well, I have leaned on the more hawkish side in both the US and UK for some time, still expecting a 2015 hike, and the BoE to be not too far behind at all, but right now I don't see anything particularly interesting in GBP rates, I mean I'll probably moan about the proxy (5y5y) terminal rate being too low (especially vis a vis USD rates) as I have done on twitter many times in the past, but ultimately its not huge, and its probably the macro economic textbooks telling me this and not what the current economy is saying.

|

| Silver |

Looking into possible long Silver vol trade.. spot in a tight range, and implieds cheap to FX composite. pic.twitter.com/htUcLhtFoM— Jere Wilkinson-Smith (@JeremyWS) May 11, 2015

USDJPY is similarly a one which we should look to position long vol in... but as I said, the summer markets may be slow so we don't want to burn premium on this just yet.

However that being said, because realized is so low, the USDJPY implied discount to the overall FX market is quite large, so premiums are cheap-ish, but still I think I'll wait till after exams

And broader Vol themes, especially in the rates market (3m5y) is heading lower, even after some larger moves in the FI space recently, and FX vols will likely track lower into the summer, assuming we don't have that June Hike, which is very very unlikely.

|

| FX vs rates vol |

The move we have seen in rates is clearly a mix between a few factors, higher inflation expectations I'm sure plays its part as I have looked at many times before, but we can't forget term premium which has moved higher, likely pushing nominal yields with them, and ya know at the same time burning a few CTAs fingers.

|

| 10Y ACM term premium |

Yup so that's pretty much it from me.. no shocking ideas or themes, which I'm glad about, hopefully I won't miss much whilst on exams :)

No comments:

Post a Comment