I've been looking at the $ returns in European assets. Below shows normalized returns of both the DAX and a basket of 10y+ EGB sovvies.

|

| DAX and EGB $ returns |

|

| DAX (inverted) vs. EURUSD |

Because of this I'd like to look at selling DAX puts, and using the premium to fund a EURUSD call. In an ideal world, I think I would look to structure this in a slightly more exotic way, maybe with some sort of x-asset KO or the such, but alas I can't. So simply selling dax put and buying a EURUSD call will make the most of both these ideas. As we looked at before, Vol In the DAX is at record levels relative to the SPX, so its potentially a wise idea to buy some deep OTM puts in SPX as a global equity hedge for this idea, but I'm not sure I'll need to pay the premium for this.

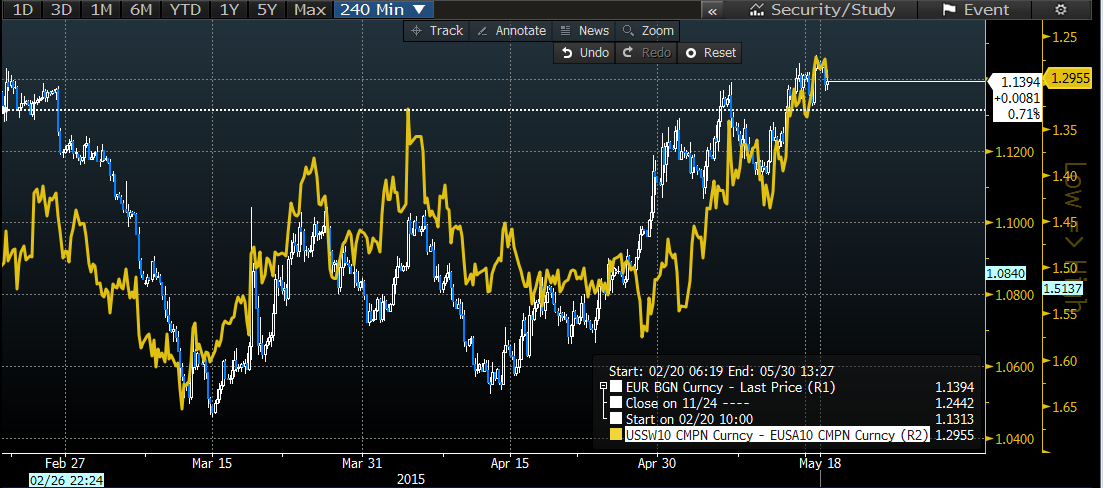

Ultimately I've been really rather happy with the EURUSD recently, buying it back in April towards 1.06, and then just 2 weeks ago in my last blog post getting bearish just shy of 1.14 - we stand pretty much at 1.10 now which seems reasonably "fair" right now, but with an upward drift bias.

That's my current play in this space, not too interesting, not much going on. NFP next week should be interesting, ultimately I don't think even if it was 300k+ we'll see a June Hike so reactions (bullish USD) could be fade potential.

In the bund space, I've only gone and recreated this stupid chart that the sell-side have adored the past few weeks..

|

| Bunds vs JGB |

Thinking more about the longer end - it does seem rather capped. We had all this excitement last month about the "taper Tantrum" part two, but that has died down rather rapidly. I like this chart which shows US 30 year swap rates overlayed with Copper. Maybe its a nice correlation, or maybe its more important that global growth prospects are the clear and present danger for higher rates, regardless of US growth. I mean after all, global rates are fairly well anchored to each other, and in think back to two weeks ago when the USD was pretty weak. Global asset managers loved picking up USD debt with the USD at such a discount especially vis a vis the EUR.

We also see Global PMIs trending lower on this chart and while I am optimistic on global growth (mostly due to higher USD / lower Oil) this downward trend will most certainly keep the long end pinned lower, especially in our low realized inflation world.

However on the shorter end, divergence is still reflected clearly. Here is a CIX of a DXY weighted 2yr swap spread of the US against the RoW. It's been a clear driver, and understandably, but its been trending lower as Fed hikes have been pushed back and back. But to me, broadly the USDs strength will be limited, and even if the spread rises, it won't support the USD as much as it has in the past. I think as we move into the hike cycle, the raw spread in support of the USD won't be as important, even now I think its importance has been overstated. At every stage, the US rates market has outperformed forwards (mostly) and we'll merely be moving along an upward sloping curve which the forwards (as calculated from the curve) see. so we could simply plug in the forwards to this and we could see a DXY 2y spread upward of 0.7% next year... but that's not to say the DXY is going to be 105+..

On the other hand, I do think that USD bearishness is limited without a major drop in this carry you now get in the dollar - its sometimes like this that I wish forwards were a predictor of price. All this time I've been bearish the USD, but its really relative to everyone's bullishness and more of a sideways drift lower in DXY.. and so I wish we could have a 1Y fwd in EURUSD under parity as per forecasts.. this would make sell-side forecasts so much more interesting :P alas, fwds are just a bit of fun maths and nothing more.

On the NZD.. since I last looked at it here where I presented the idea that the RBNZ could cut rates. Since then some smaller banks have agreed with me, and more recently HSBC have thought this is possible. More importantly the NZD TWI has dropped from 160 to 149, and the crucial cross with AUD has pulled back a lot, but still high.

|

| NZDAUD |

Carry/vol is also a great indicator for NZD - and both don't paint a pretty picture. Carry has dropped remarkably as the market has seen the turnaround in the RBNZ rhetoric.

|

| Carry/vol vs NZDUSD |

|

| Taylor Rule for New Zealand |

Here we can see the Taylor rule for NZ.. now I know all the arguments for/against this.. but we can see quantitatively the justification for lower rates, maybe not 0.75% of course, but lower - lets say 3%. Still we'll see, I'm not 100% sure they'll cut at the next meeting, and I'm not even short the NZD anymore, I've taken it for its ride and am happy, but the concern for us is the positioning is heavily short and we appear to be quite overextended, so by no means would I want to short here, bounces, maybe...

Still not too many idea, Exams probably have a part to play in that, but im nearly done and I'm sure the twitter/blog flow will pick up :)

Thanks for reading y'all